Institutional Insights: Goldman Sachs Delta One' Asia, Oil, AI, CPI, & Risk'

Asia, Oil, AI, CPI, and Risk: The Market Is Testing the AI-Capex Trade

The overnight and pre-CPI setup reinforces the current market framework: the bull market may remain intact, but the dominant marginal risk is now a positioning flush in AI / semis / high-beta momentum, not a broad macro liquidation. Asia was weak, Korea reversed sharply, oil is refusing to respond to geopolitical escalation, CPI is the immediate macro catalyst, and the AI investment debate is becoming more two-sided as investors reassess where inference demand ultimately resides.

## 1. Asia: Hardware/Semi Unwind Spills Globally

Asia had a poor session, with Korea down 4.5%, though it bounced off the lows. This matters because Korea is one of the cleanest global expressions of the semiconductor, memory, hardware, and AI supply-chain trade. When Korea sells off this aggressively after a strong prior session, it suggests the global AI hardware trade remains unstable.

The move appears less about a single regional catalyst and more about the broader unwind in global semis and hardware. Leverage is compounding the move. That is the key phrase. When exposure has been built through high-beta stocks, options, levered ETFs, swaps, and crowded hedge-fund books, relatively small pieces of negative news can produce outsized price action.

China inflation data were broadly in line, with PPI running at its hottest level since 2022. That adds to the global reflation narrative, though it does not appear to be the dominant driver of the equity tape. In Japan, a weak JGB auction pushed rates marginally higher, but again the main equity issue is not really Asia rates. It is the global reassessment of AI-linked positioning.

## 2. Oil: Headlines Bullish, Price Action Bearish

Oil remains one of the most important cross-asset tells. A lot has been thrown at the oil market, including continued geopolitical escalation, but crude is simply not going up. In fact, WTI was down roughly 3% in the prior US session despite a ceasefire walk-back and Trump vowing to respond to the Apache downing.

The most rational conclusion is that barrels are still getting through the Strait of Hormuz, visibly or otherwise. If that is correct, then Iran’s leverage over global energy markets may be lower than many assumed. Without a credible mechanism to materially disrupt flows, the geopolitical risk premium becomes difficult to sustain.

That does not mean the geopolitical risk is irrelevant. It means the oil market is demanding evidence of actual supply disruption, not just escalation headlines. The market seems to be saying: rhetoric and tactical conflict are not enough; physical barrels need to be impaired.

The practical tripwires are therefore clear:

1. Iran strikes energy infrastructure outside its borders, especially Gulf production, export, or processing assets.

2. US actions move beyond tactical degradation and toward regime-change objectives, which would raise the probability of broader regional disruption.

Until one of those occurs, oil price action remains bearish even if the headlines remain alarming. That is important for equities because lower oil helps contain the inflation shock and reduces the risk of a stagflationary impulse.

## 3. Bimodal AI: Frontier Cloud vs Local/Open AI

The AI debate is evolving. Frontier models continue to improve rapidly. Quality, usefulness, and reasoning capabilities are all moving higher. But AI increasingly appears to be splitting into two worlds.

### The first world: premium frontier intelligence

This is centralized, cloud-based, expensive, and compute-intensive. It includes frontier models, advanced reasoning, agentic workflows, enterprise-grade inference, and eventual superintelligence or AGI-adjacent capabilities. This world supports massive spending on:

- Data centers

- GPUs and accelerators

- HBM and memory

- Networking

- Power and cooling

- Cloud infrastructure

- Security and data architecture

### The second world: local and open AI

The second world is free or nearly free, open, increasingly capable, and local. These models can handle a large percentage of everyday tasks. They may run on existing devices or relatively modest incremental hardware, especially as models become smaller, more efficient, and more specialized.

The likely end state is bimodal:

- Basic work is handled locally or by open models.

- Complex reasoning and difficult problem-solving are delegated to premium cloud-based systems.

This is a major investment question because it determines where the economics of inference accrue.

## 4. The AI Investment Debate: Bigger Pie or Overbuild?

The implications for the AI investment cycle are genuinely unclear. There are two credible interpretations.

### Bullish interpretation: the pie gets much bigger

In the bullish version, AI demand expands dramatically across both frontier and local use cases. Smaller models democratize usage, frontier models unlock new high-value workflows, and the total amount of inference explodes. That requires more:

- Edge compute

- Data centers

- Memory

- Power

- Networking

- Cooling

- Storage

- Security

- Data infrastructure

In this version, efficiency does not reduce total compute demand; it expands the addressable market. This is similar to Jevons paradox: as the cost of compute falls, usage rises even more.

### Bearish interpretation: useful tasks migrate to cheaper compute

In the bearish version, many economically useful AI tasks can soon run locally, on open models, or on existing hardware. If that happens, demand for premium cloud inference may take longer to inflect than current valuations imply.

This does not mean AI is fake or model quality is poor. Quite the opposite: model quality may be improving so quickly that expensive centralized inference becomes necessary only for a smaller set of complex tasks. The investment debate is therefore shifting from “will AI work?” to “where will inference ultimately reside?”

That is a much more dangerous question for the market because valuations in parts of the AI supply chain assume a very large and persistent centralized infrastructure buildout.

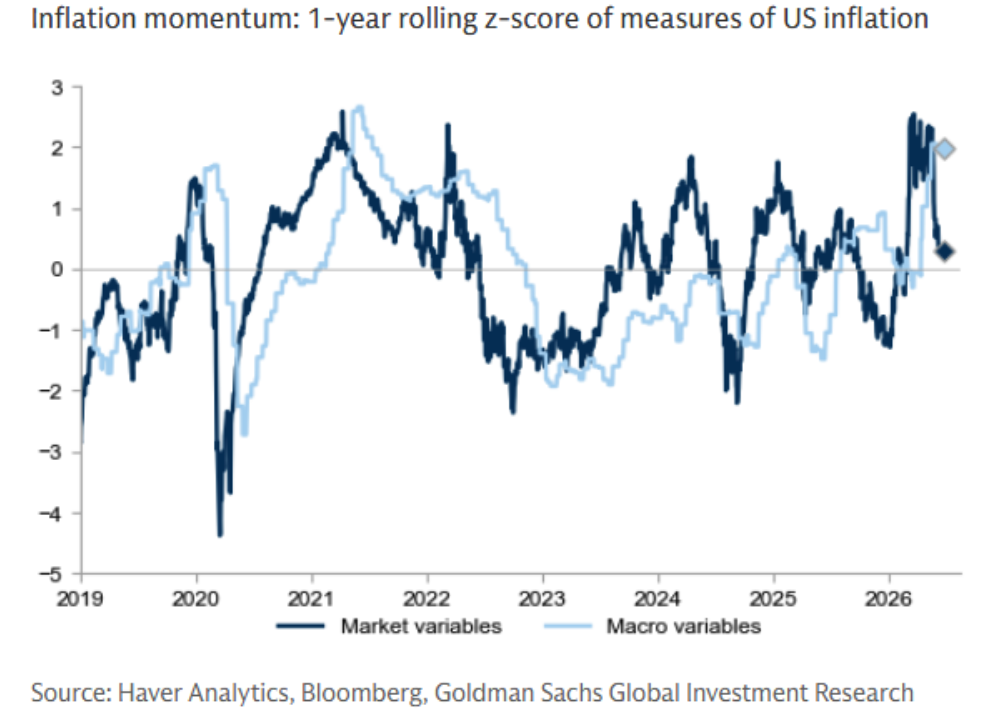

## 5. CPI: Official Data Benign, Inflation Narrative Still Hot

All eyes are on US CPI. Consensus expects core CPI around 0.3% month over month and 2.9% year over year. GIR is below consensus, expecting a 0.17% increase in May core CPI, corresponding to 2.79% year over year.

A soft CPI print would matter because the market has become highly sensitive to rates volatility. A benign core print could calm yields, reduce pressure on long-duration growth, and stabilize the AI / Tech unwind. It would also reinforce the idea that inflation remains contained despite scary headlines.

But from a practical standpoint, inflationary forces remain powerful. Headline inflation is cited around 4.2% year over year, and the economy has several sources of nominal heat:

- Higher energy costs, even if crude has recently failed to rally

- Nearly a trillion dollars of AI-related corporate investment

- A US fiscal deficit around 6–7% of GDP

- Strong labor markets

- Easy financial conditions

- Ongoing capex and infrastructure demand

This is an investment-led economy running hot. Inflation may remain a byproduct unless productivity accelerates materially. AI-driven productivity is the potential escape valve. Without it, strong nominal growth can keep inflation sticky and constrain the Fed.

## 6. Risk: Nasdaq Selloff Was a Positioning Warning

The Nasdaq selloff was sharp and caught many off guard because there was no obvious single catalyst. The Crusoe data-center delay likely mattered at the margin because the market is hypersensitive to any sign that AI capex may be delayed, deferred, or reprioritized.

The details are important. Crusoe reportedly paused a 1.8 GW Wyoming data-center project at the request of its customer. The project was notable because it had been designed to bypass grid bottlenecks with 900 MW of behind-the-meter energy sources. The site had barely begun development, and the customer remains undisclosed, so it would be a mistake to draw broad conclusions.

Still, in the current market, isolated data-center delays can have an outsized psychological impact. Everything is tied to AI capex: semis, memory, networking, power, utilities, construction, industrial equipment, private credit, GDP growth, and equity-index leadership. If investors start questioning the durability or timing of the AI spending cycle, the vulnerability is obvious.

The broader issue is positioning:

- Momentum returns are in the 90th percentile.

- Gross exposure is in the 99th percentile on a five-year lookback.

- Funding spreads have widened as demand for leverage has increased.

- Retail participation through leveraged ETFs remains substantial.

- Net allocation to semis remains near five-plus-year highs.

- AI is embedded across both cash and synthetic exposures.

That combination creates circularity. AI spending drives economic growth and market performance. Market performance supports capital formation and confidence. Capital formation supports more AI spending. If one part of that loop breaks, the unwind can become self-reinforcing.

## 7. Why Gamma Has More Utility Here

Given the amount of embedded and synthetic exposure created by leveraged products, owning gamma has more portfolio utility than many appreciate. The issue is not simply downside risk. It is path risk.

The market can gap lower on small pieces of negative AI capex news because positioning is crowded. It can then snap back on soft CPI, lower yields, buybacks, or dip-buying. This kind of environment rewards convexity. Long gamma helps portfolios manage both downside air pockets and sharp reversals.

This fits the existing tactical framework:

- Stay long the primary bull trend.

- Rotate toward less crowded sectors.

- Maintain high-conviction liquid longs.

- Use puts or other convex hedges to protect against positioning flushes.

- Avoid assuming that low realized index volatility means low risk under the surface.

The immediate setup is fragile but not broken. Asia weakness, especially Korea, confirms that the global semiconductor and hardware trade remains under pressure. Oil’s failure to rally despite geopolitical escalation is a bearish signal for crude and a modest relief valve for inflation, unless actual energy infrastructure is hit or US objectives escalate toward regime change.

The bigger market issue is AI circularity. The AI investment cycle is still structurally powerful, but the market is now debating whether inference demand will remain centralized and infrastructure-heavy or migrate toward smaller, cheaper, local models. That debate matters because positioning in AI hardware, semis, and momentum is extremely crowded.

CPI is the near-term catalyst. A soft print could stabilize rates and support a Tech bounce. A hot print could intensify the positioning flush. Either way, the tactical conclusion remains the same: stay constructively long the bull market, but own gamma and downside protection because the AI trade is crowded, levered, and increasingly sensitive to any challenge to capex assumptions.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!